SPX Greek Hedging

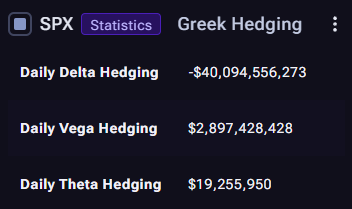

Greek Hedging (SPX) estimates the day’s dealer rebalancing flows implied by the current options book essentially how much trading may be required for dealers to remain hedged as prices and volatility move.

Here the dominant signal is Delta hedging (-$40.1B), indicating very large price-linked hedging flows that could require dealers to sell underlying exposure as the market moves, pointing to significant sensitivity to spot price changes. Vega hedging ($2.90B) shows meaningful exposure to shifts in implied volatility, meaning volatility changes could also drive additional hedging adjustments. Theta ($19M) reflects the smaller, steady impact from time decay as options gradually lose value.

Source: Vol.land