Credit Ágricole: Rates - FJElite

- Market narrative shifts to stable energy prices supporting the front end. Curve dislocations should correct over the short term.

- Central bank meetings dominate this week, with high focus on potential hawkish tone amid energy-driven uncertainty.

- We look at EUR rates implications for the five scenarios highlighted by our inflation and macro teams. Tomorrow’s ECB meeting will help assess the relative probability of each scenario.

- Markets will focus on the FOMC meeting today, where we expect the Fed to extend its pause for another meeting. Forward guidance will likely remain unchanged, with Chair Jerome Powell likely reiterating that policy is currently "well positioned", leaving all options on the table.

- In relative value, 20Y Treasury bond has underperformed vs 10Y and 30Y since late January. The cheapening has accelerated since the start of the Iran war.

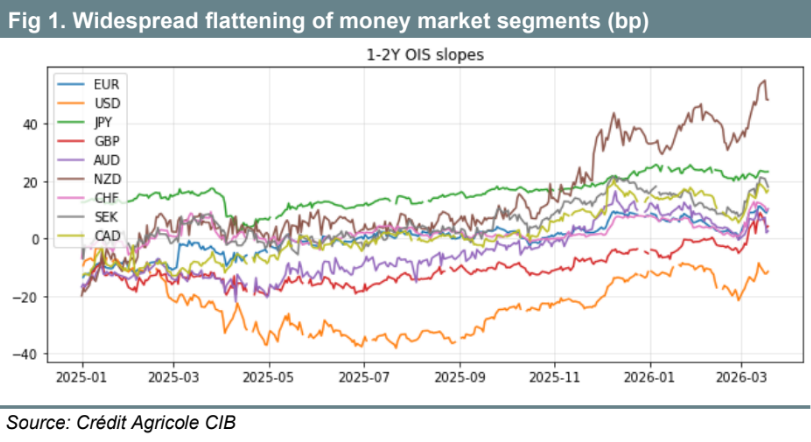

Stable energy prices are a key factor to move away from pure energy inflation expectation chasing a more composed search for the new equilibrium. While energy prices remain elevated, their volatility has declined, providing support for short-dated contracts across most G10 currencies (Figure 1). We maintain that the cumulative nature of this supply shock will prevent significant repricing until there is any clarity on the duration of the war in Iran. However, with positioning constraints no longer a major factor, pricing should begin to better reflect the range of possible scenarios rather than binary outcomes driven solely by energy prices. This creates an opportune window to address curve distortions, though it is premature to establish strong directional bets.

A

Markets will focus on central bank meetings all week, in particular the FOMC today, where we expect the Fed to extend its pause for another meeting. Forward guidance will likely remain unchanged, with Chair Jerome Powell likely reiterating that policy is currently “well positioned', leaving all options on the table. Given the high level of uncertainty, the Summary of Economic Projections (SEP) may see limited changes, a trend we also expect for most of the central banks, given the path-dependent nature of energy price percolations into inflation expectations and central bank reaction functions. The main area to monitor in Europe will be how hawkish the ECB communication will turn out.