Deutsche Bank: Why the Dollar Still Faces Medium-Term Downside Risk - FJElite

Two common claims around the US balance of payments are often seen as dollar-positive, but both look weaker on closer inspection.

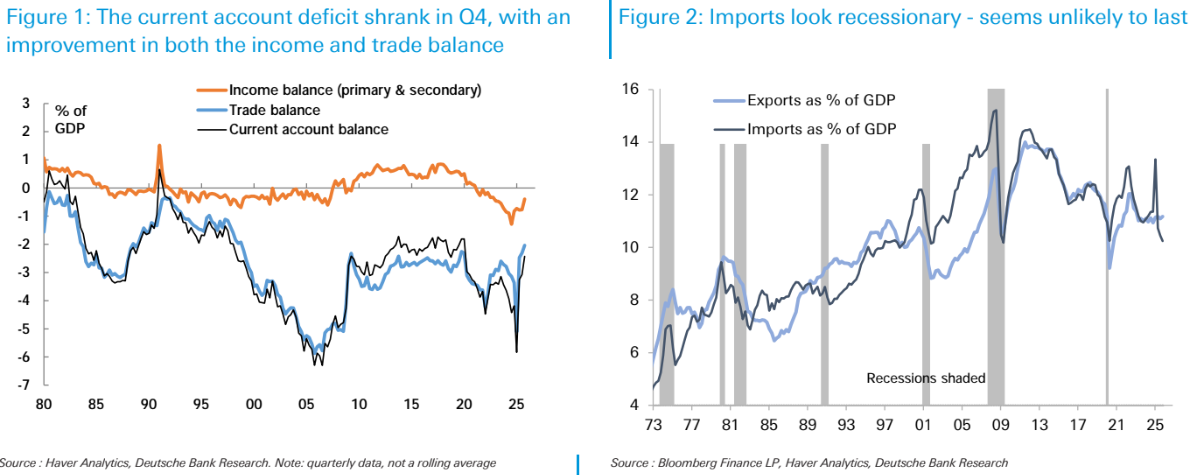

The first is that the trade and current account deficit has narrowed sharply. That is technically true, with the current account deficit falling to around 2.5% of GDP in Q4, a six-year low, but the improvement looks misleading. Much of it came from an unusual surge in the income balance, entirely driven by FDI income, which tends to be lumpy and could easily reverse. The narrowing in the trade deficit also looks more like payback from the import surge in the first half of 2025 than a lasting structural improvement. On an annual average basis, the current account deficit is still above 3% of GDP and remains one of the largest in the G10.

The second claim is that the world will continue to fund the US external deficit because there is no real alternative to buying US debt. That story looks increasingly outdated. Over the past year, net equity inflows have been almost as large as net debt inflows, which is unusual and has significantly increased foreign exposure to US equities. Foreign investors now hold around 30% more in US equities than in US fixed income, leaving them more exposed to valuation shifts and relative equity performance than before.

That matters because foreigners built up US equity exposure just as US equities started to underperform many other markets. If that begins to surprise investors, it could lead to rebalancing away from the US rather than continued support for the dollar. The broader takeaway is that the recent improvement in the external accounts may not be as durable as it looks, while the financing side is no longer as clearly supportive as it once was, leaving medium-term downside risk for the dollar.