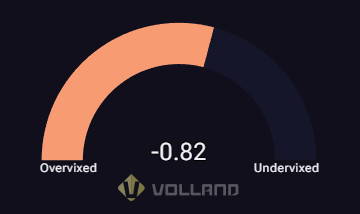

SPX Spot-Vol Beta: -0.82

This gauge measures how implied volatility (via the VIX) is reacting relative to the S&P 500’s price move. A reading of -0.82 suggests volatility is under-reacting, meaning options traders are not aggressively bidding up protection despite the underlying market move. This points to a relatively muted demand for hedging compared to the price action.

Spot-vol beta reflects how much volatility is over- or under-reacting to changes in the S&P 500’s spot price.

Source: vol.land