MUFG: USD Monthly - FJElite

Market Update

In March the US dollar strengthened notably against the euro in terms of London closing rates, from 1.1818 to 1.1524. The dollar strengthened by less against the yen, from 156.05 to 159.00. The FOMC at its meeting in March kept the range for the federal funds unchanged at 3.75%-4.00%. The FOMC confirmed the end of QT effective December last year with the Fed no longer reducing UST bond holdings by USD 5bn per month. MBS holdings would continue to decline but would be offset by buying of US T-bills, initially amounting to around USD 40bn per month.

Outlook

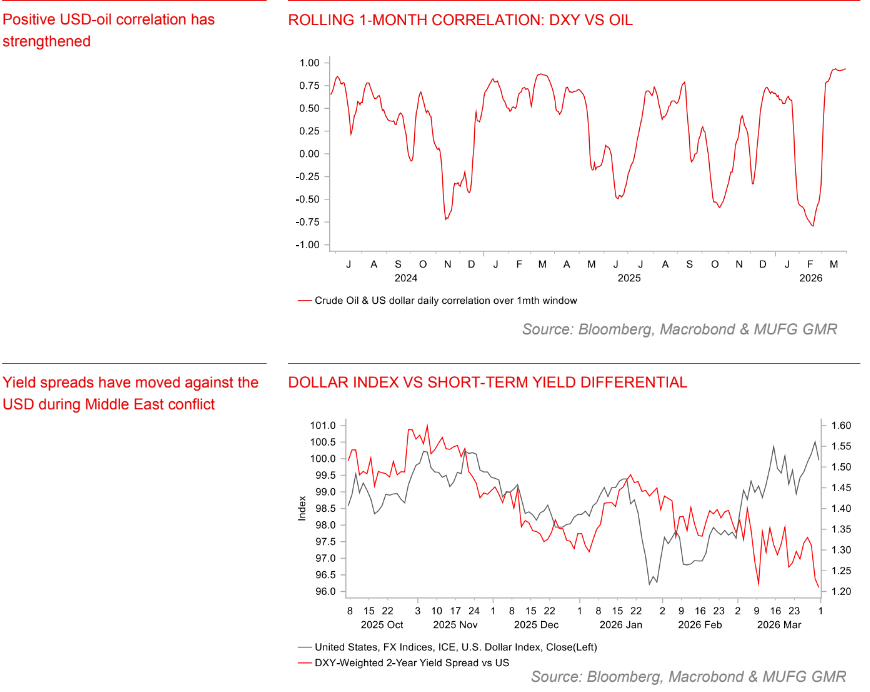

The US dollar, on a DXY basis, advanced in March by 2.4%. The start of the conflict in the Middle East resulted in a surge in energy prices with Brent crude oil up 44% at the end of March and TTF natural gas up 59%. The daily correlation on a 1-month rolling basis between the percentage change in crude oil and the dollar has strengthened notably although the scale of US dollar strength is a little less than would have been expected based on our regression analysis of previous oil price spikes over the post-shale oil period (since 2012) which indicates that the US dollar should be stronger. Hope of peace may be playing a role here with FX responding to President Trump's comments that peace negotiations have begun.

The terms of trade driver of FX was not that apparent in G10 FX performance in March with intervention threat and yield playing a role. After the USD, JPY, GBP and NOK are three of the best performing G10 currencies. But the scale of depreciation versus the US dollar is likely being limited by concerns over the health of the US economy. The 92k drop in NFP in February highlights the fragility of the US economy and will limit terms of trade benefits. The average retail gasoline price has surged 34% since the crisis began, which will drag on consumer confidence and spending. Furthermore, investors are likely confused over the strategic goals with the White House communicating different goals and no clear strategy that could ultimately undermine confidence in US assets over time. The suggestion at the end of March of US de-escalation without a clear resolution to the Strait of Hormuz and possibly without a deal with Iran and the regime left intact we believe will likely reinforce the potential for a further loss of confidence in US assets.

In a severe scenario, the conflict drags on and attacks on energy production infrastructure increase in scale which extends the timeline of supply disruption. Brent crude oil could then trade in a higher range of USD 120-160p/bl that results in increased risks of global recession. Equity markets fall more sharply and the ToT and yield dynamic impacting FX fades and there is a stronger initial flight to the US dollar. The DXY in this scenario could extend higher up to the 105-level. In a scenario that at the time of writing is becoming more plausible, a half-hearted de-escalation with uncertainties persisting over the Strait of Hormuz and instability in the Middle East will undermine confidence in the US and hence in US assets and the dollar.

Interest Rates Outlook

Given the high uncertainty, a scenario based framework is the most appropriate lens to analyze the macro situation. In the best-case, a quick resolution to the war and the reopening of the Strait of Hormuz would allow oil prices to drift down toward preconflict levels ($50-$75). If the labor market shows signs of stabilizing, it could delay or reduce the total amount of rate cuts. Our base case is more pessimistic and assumes a longer conflict (a series of ceasefires/negotiations) with oil hovering in the $75-$100 range. This would likely offset some or most of the Q1 boost from OBBBA related tax refunds, softening the growth outlook and making unemployment risks outweigh inflation risks. As long as inflation expectations remain anchored with oil below $100, the Fed should see past the oil driven supply shock and begin normalizing policy, thus we keep our three cuts, starting in July. In the worst-case, oil prices hold above $100 and become a significant macro headwind, tightening financial conditions as equities reprice to weaker earnings. Oil this high would initially create a stagflationary shock that could evolve into a recession risk, particularly if private credit markets continue to deteriorate in the background.(George Gonçalves)