Citi's Review of US Last Week - FJElite

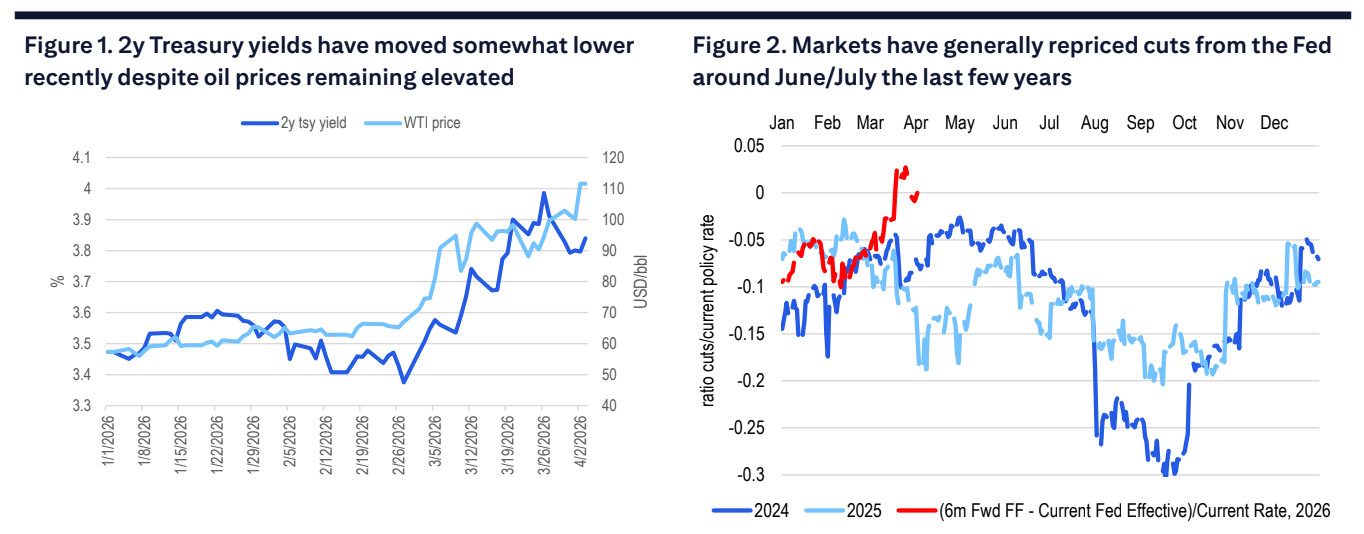

Developments affecting energy prices continue to be the dominant force driving global markets despite more economic data released this week. Even market reactions to a very strong 178k jobs added in March were somewhat muted, with 2- year Treasury yields moving around 5bp higher.

Oil prices rose as the specifics on a path towards resolution of Middle East disruptions remain unclear. But rather than a substantial move higher in yields on concerns of higher inflation, interest rate markets have shifted more towards balancing downward growth implications from higher oil prices with upside inflation risks. Fed officials will feel very comfortable keeping rates on hold for now following the strong March jobs report, with markets pricing rates essentially unchanged through the year.

We continue to think signs of a weakening labor market will result in cuts later in the year. But timing of upcoming data suggest a later start to rate cuts than we had previously been expecting. We now expect 75bp of cuts this year starting in September (September, October, and December meetings), also a very similar pattern to recent years.