SPX Greek Hedging

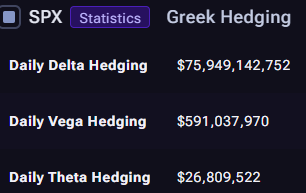

Greek Hedging (SPX) estimates the day’s dealer rebalancing flows implied by the current options book essentially how much trading may be required for dealers to remain hedged as prices and volatility move.

Here the dominant signal is Delta hedging ($75.9B), pointing to very large price-linked hedging activity that may require dealers to buy underlying exposure as prices move, reinforcing directional momentum. Vega hedging ($591M) indicates modest sensitivity to changes in implied volatility, suggesting volatility-driven hedging flows are present but secondary. Theta ($26.8M) represents the steady impact from time decay, relatively small compared to the larger delta dynamics.

Source: Vol.land