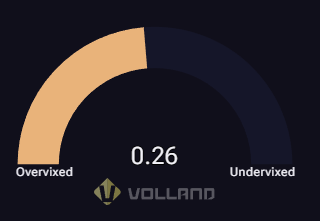

SPX Spot-Vol Beta: 0.26

This gauge measures how implied volatility (via the VIX) is reacting relative to the S&P 500’s price move. A reading of 0.26 suggests volatility is slightly overreacting, meaning options traders are bidding up protection somewhat more than the underlying price move would imply. The divergence is modest, indicating only a mild increase in hedging demand.

Spot-vol beta reflects how much volatility is over- or under-reacting to changes in the S&P 500’s spot price.

Source: vol.land