MUFG: The JPY - FJElite

The yen has strengthened modestly overnight following the BoJ's latest policy meeting resulting in USD/JPY dropping back below the 159.00-level. The BoJ decided to leave the policy unchanged as expected at 0.75% but the decision was not unanimous. There were three dissenters who voted for a rate hike today which was the biggest opposition to a policy decision under Governor Ueda. Hajime Takata was joined by Junko Nakagawa and Naoki Tamura in voting for a rate hike. Hajime Takata had previously voted for rate hike in both January and March. Hajime Takata considered that the price stability target had been more or less achieved and that risks to prices in Japan were already skewed to the upside due to second-round effects of price rises stemming from overseas developments. Junko Nakagawa considered that, while the situation in the Middle East remained unclear, given economic developments, risks to prices were skewed to the upside under accommodative financial conditions. Naoki Tamura considered, with risks to prices becoming significantly skewed to the upside, the Bank should set the policy interest rate as close to neutral as possible. The vote for a hike from Junko Nakagawa was more of a surprise as she has not previously signalled a particularly hawkish policy stance, although her term Is due to end In June. The hawkish voting pattern has encouraged Japanese rate market participants to pnce in a higher probability of the BoJ hiking rates at the next policy meeting m June

At the same time, the hawkish repricing of BoJ rate hike expectations has been encouraged by the significant upward revisions to the inflation forecasts. The updated Outlook for Economic Activity and Prices report revealed that the median forecasts for headline and core inflation were revised higher both for the current and following fiscal years. The headline inflation forecast for FY2026 was revised higher by 0.9ppts to 2.8% and more modestly by 0.3ppts to 2.3% for FY2027. Headline inflation is then expected to fall back to target at 2.0% in FY2028. The core inflation forecast for FY2026 was revised higher by 0 4ppts to 2.6% and by 0 5ppts to 2 6% for FY2027. The projected timing for achieving the pnce stability target was left unchanged as dunng the latter half of FY2026 through to FY2027. The BoJ added in the Outlook report that it is necessary to pay particular attention to the impact of the future course of the situation in the Middle East on financial and foreign exchange markets and on Japan's economic activity and prices. The BoJ Judges that nsks to prices are skewed to the upside particularly for FY2026. and it is necessary to pay due attention to keep the risk of inflation significantly deviating to the upside from materializing and exerting an adverse impact on the economy. On the other hand, the BoJ judges that risks are skewed to the downside for economic activity. The forecast for growth in FY2026 was revised down by 0.5ppt to 0.5% and by 0.1 ppt to 0.7% for FY2027.

In the accompanying press conference, comments from Governor Ueda sounded less hawkish. He noted that uncertainty remains over the Middle East situation which has made the BoJ cautious over hiking rates further in the near-term. He indicated that the BoJ will be watching the impact from the Middle East conflict on FX. the economy and pnces. Recent negative developments have made Governor Ueda a lot less confident that their baseline economic outlook will be realized while adding he'll be watching to see if the likelihood rises again. He added that the BoJ wants more time to assess Middle East developments and impact on pnces more, and will make appropriate decision from next month. He reiterated that further rate hikes will depend on the economic situation. He emphasized that the three dissents for hike today will be taken seriously which reflect the difficulty in assessing the npact of supply shocks. He stressed that the BoJ needs to hike if the supply shock affects underlying inflation At present the other board members don’t see the need for action now. He believes that it is not yet clear if economic or price risks will appear first. Overall, he refrained from providing a strong signal that a hike will be delivered as soon as June.

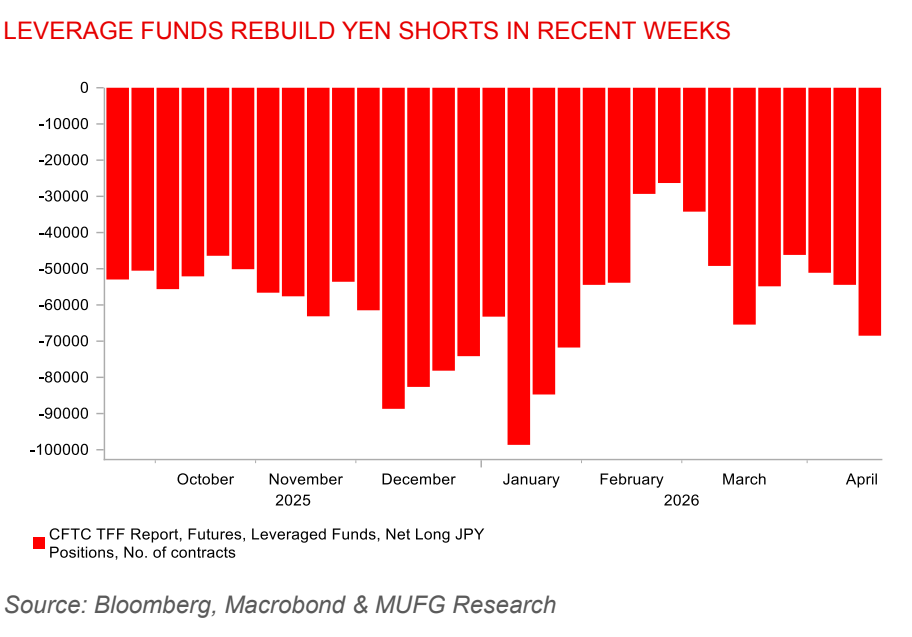

While today's hawkish hold from the BoJ has helped to provide support for the yen. it is unlikely to trigger a sustained reversal of the bearish trend that has been in place since the Middle East conflict started in late February. The yen has been one of the worst performing G10 currencies dunng the conflict alongside the Swedish krona and Swiss franc. The combination of still buoyant global investor nsk sentiment alongside the deterioration in Japan s terms of trade have encouraged a weaker yen. The latest IMM report revealed that leveraged funds have been rebuilding short yen positions in recent weeks. The unfavourable developments are keeping pressure on Japan to back up their verbal intervention threats if they want to prevent the yen from weakening further In the near-term. Finance Minister Katayama delivered another warning today ahead the BoJ's policy meeting to deter speculative seling by stating that *l have consistently referred to taking bold action when needed." When asked whether the government remains on alert as Japan prepared to enter the Golden Week holiday period, she replied "we’re ready to respond 24 hours a day*. She remains of the view that volatility in crude oil futures remains elevated, and is seen as fuelling speculative moves in the yen.