Volland SPX Greek Hedging

Volland SPX Greek Hedging

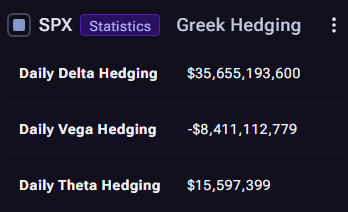

Greek Hedging (SPX) estimates the direction and size of daily dealer rebalancing flows implied by the options market.

Delta hedging (~$35.66B): suggests dealers may need to buy underlying (or futures) to stay hedged against price moves, implying potentially strong flow impact.

Vega hedging (~-$8.41B): exposure to changes in implied volatility; typically managed through repricing options, with the negative figure indicating declining volatility sensitivity.

Theta hedging (~$15.60M): the impact of one day passing on the dealer book; like vega, this is largely handled through option repricing, with time decay adding modestly to hedging needs.

Greek hedging: net notional dealer hedging that needs to be applied by the end of the day @wizofops

Source: vol.land