Goldman Sachs on the AI Trade - FJElite

AI capex surprises and spreading fears of disruption risk have injected new volatility into the AI trade in recent weeks. Memory stocks have rallied by an average of 55% YTD while software stocks have plunged by 24%.

We expect modest further upside to consensus hyperscaler capex estimates but continue to expect a peak in the capex growth rate later this year. Consensus estimates show hyperscaler capex growing to $667 billion in 2026, $127 billion higher than at the start of the 4Q earnings season and 62% growth vs. 2025. Hyperscaler capex is now on pace to exceed 90% of cash flows this year, above the share during the Dot Com Boom. Our previous upside capex scenario equaled roughly $700 billion. However, even in that outcome, a deceleration in the quarterly growth rate is likely in late 2026. The revenue growth and valuations of some AI infrastructure stocks appear vulnerable to a slowdown in capex growth. Even where rallies have been driven entirely due to earnings, the recent dislocation between NVDA price and earnings shows the challenges of delivering persistently strong returns amid fears of “over-earning.”

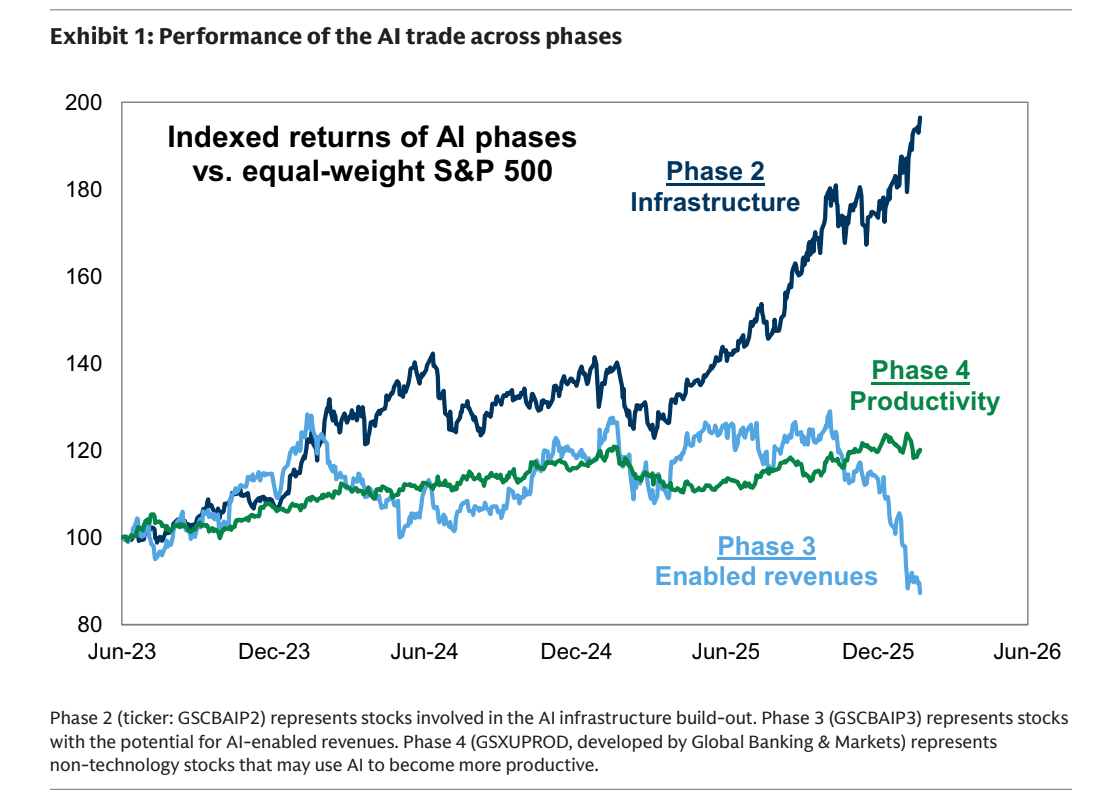

In recent weeks, the AI trade has been upended by large capex surprises and investor focus on the risk of disruption. “Phase 2” AI infrastructure stocks have continued to perform well alongside strong capex guidance from the hyperscalers during 4Q earnings season. At the same time, “Phase 3” companies with the potential to generate Al-enabled revenues have suffered as investors have priced growing risk from AI disruption. “Phase 4” companies outside of tech that could potentially benefit from AI productivity gains have traded roughly sideways during the past few months.