Credit Ágricole: US May Jobs Data - FJElite

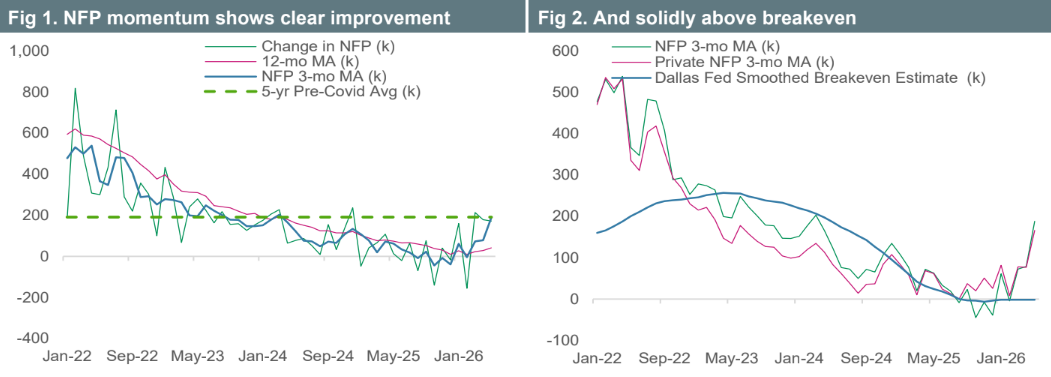

- The May jobs report extended a string of strong reports into a third month, led by a substantial upside surprise for NFP. The jobs data continues to exhibit a clear improvement compared to last autumn, and at this point hints at the possibility of a re-acceleration as opposed to just stabilisation.

- The NFP figure jumped off the page right away, printing at +172k to come in well above not only the consensus of +88k but even the highest forecast in the BBG survey. While technically a deceleration compared to +179k in April, this is still a strong print in the current environment in which the breakeven pace has likely dropped sharply.

- Furthermore, both March and April were revised higher as two-month net revisions totalled +93k, driving the three-month moving average to its highest level in more than two years at +188k. If we were to nitpick, we would note that private NFP were softer than headline and gains were relatively concentrated in a few sectors, though this is not nearly enough to outweigh the strength of the headline number and revisions.

- The unemployment rate held steady at 4.3%, remaining at a historically low level that sits below the 4.5% print in November. Household survey details were solid as well, with household survey employment bouncing back from a couple of soft months at +149k, outweighing a slight uptick in the size of the labour force to see the unrounded unemployment rate tick down a few bp to 4.30% from 4.34%.

- AHE were firmer on a MoM basis at 0.3% MoM compared to 0.2% MoM in April, though the YoY rate ticked down to 3.4% from 3.6%. This would do nothing to dissuade the Fed from the view that the labour market is not a major source of inflationary pressure at the moment, despite the strong job gains.

- For the Fed, another strong report bolsters the view that the labour market has stabilised, quashing any lingering thoughts of a rate cut this year (if there were any still out there). That said, we are not entirely convinced that today's report changes all that much when it comes to the possibility of a rate hike. If the Fed does hike, it will come down to inflation, meaning next week's inflation data will likely play a larger role in the Fed’s near-term decision-making process than the jobs data.