Official Statement

The official statement was much shorter than usual; an indication Warsh is already making his mark. The statement also removed the language that suggested an easing bias (which was the reason for dissents in April), as was expected. The statement concludes with a commitment that the FOMC will “deliver price stability."

The statement also excludes the names of the voting participants in the meeting. It is unclear as of now if this will continue if there are dissents in the future.

Summary of Economic Projections

Similarly, the Summary of Economic Projections shifted in a much more hawkish direction. There are nine participants now expecting a hike by the end of the year, with the median dot showing a cut in 2027 and another in 2028.

The SEP downgraded growth to 2.2% (from 2.4%) and massively upgraded expectations for core inflation to 3.3% (from 2.7%). Meanwhile expectations for the unemployment rate fell to 4.3% (from 4.4%). The increase in inflation expectations and half the participants expecting a hike is a very hawkish development and shows that the reaction function of the FOMC may be more sensitive to rising inflation.

Further out however, the median dot expects an end 2027 policy rate of 3.6% (one cut), with another cut penciled in for 2028.

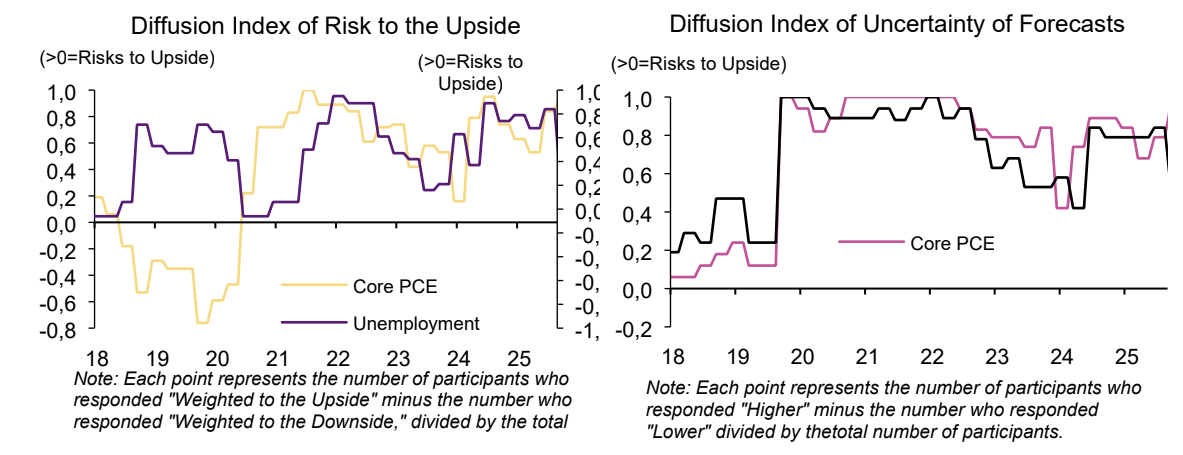

The Uncertainty Diffusion Index showed that, compared to March, fewer participants now see higher uncertainty and downside risk around their real GDP growth projections. For the unemployment rate, more participants judge the risks to their projections as broadly balanced, as those who had previously noted upside risk declined. For core PCE inflation, the number of participants seeing upside risks to their inflation projections increased and includes almost all participants.

Press Conference

Though Warsh was a staunch advocate of lower rates given his optimism about the disinflationary impact of productivity gains from artificial intelligence, his prepared statement was unambiguously hawkish. He doubled down on the notion that “inflation is a choice" and that forward guidance is not an appropriate tool.

Warsh seems ready to buck the Fed/market feedback loop where the market digests Fed communication. Instead, he seems to want more price discovery from markets and for the Fed to digest markets’ interpretation of economic developments.

On the current policy stance, Warsh commented that it appears to be restrictive when looking at the housing market, but that he cannot say the same when looking at asset markets. On inflation, he underlined that the Entire Committee is firmly committed to achieving price stability, noting that inflation has not been at target in five years, and that he does not appear to have much more tolerance for inflation. On employment, Warsh noted that job gains have kept pace with the workforce and that the unemployment rate has changed little.

As before the press conference, Warsh was vocal about the changes he would like to bring to the Fed communication. He noted that forward guidance is not well suited in the current environment and emphasized that the dots will be reassessed in the coming months. He also indicated that the current dots represent the modal forecasts, but nothing that is conclusive. According to Warsh, press conferences can be a useful way to communicate, but to be used when communicating something important.

Warsh also indicated that more changes are on the way. We said he is assembling a task force to investigate changes in the following areas: a) communication b) balance sheet, c) data utilization, d) productivity and jobs and e) inflation framework.

What to expect going forward?

Because of the elevated energy costs and prolonged uncertainty, we think the Fed will require additional proof that the energy shock is contained primarily to headline prices. Higher headline inflation prints were to be expected when the war began and some passthrough to core inflation was expected as well for energy-intensive products.

The question is will the Fed "look through" supply side shocks? We thought that if inflation was heading down, even if not at target, the Fed would pivot to a more dovish stance. After the developments from today, we aren’t so sure.

There indeed may be, as Warsh intimated during his confirmation hearing, less tolerance for inflation regardless of the reason. That is certainly an increased possibility now given that half the participants are now expecting a hike by the end of the year. We are still cautiously optimistic that the trajectory for inflation will be downward towards the end of the year. If that is the case, the Fed could still cut, but if inflation proves sticky, we think an extended pause would be appropriate.

US Rates Strategy - Initial reaction

With the results of the June FOMC meeting more hawkish than expected, we are closing our 2yr long established June 8 at an average of 4.15% for a scratch. We do think the pricing of ~32bps by year end is enough for now, and we also think the market pricing in more than two hikes total will be tough sledding, but even so we believe it will be difficult for the market to rally significantly in the face of Warsh's clear focus on price stability. Said another way, it may take an accumulation of positive inflation data for a meaningful rally and in the least we’ve certainly reset the range higher given the Fed statement and Warsh’s comments. On curve, much of the same follows - the reset flatter makes sense as long as the Fed appears more focused on price stability and may struggle to steepen until we see better inflation data. We do like owning market inflation on dips for longer term reasons, and think scaling into inflation hedges from here makes some sense given it’s declines on the more hawkish Fed.