Credit Ágicole: FX Weekly - FJElite

- The signing of the MoU between the US and Iran to reopen the Strait of Hormuz and extend their ceasefire by 60 days has already led to a bounce in investor sentiment. The Brent crude oil price is below USD80/bl for the first time in three months and investors are reducing their central bank rate hike expectations supporting global equity markets. The MoU has eroded the USD’s safe-haven and energy price appeal. This appeal would quickly return, however, if the 60-day ceasefire failed to lead to a deal on Iran's nuclear programme.

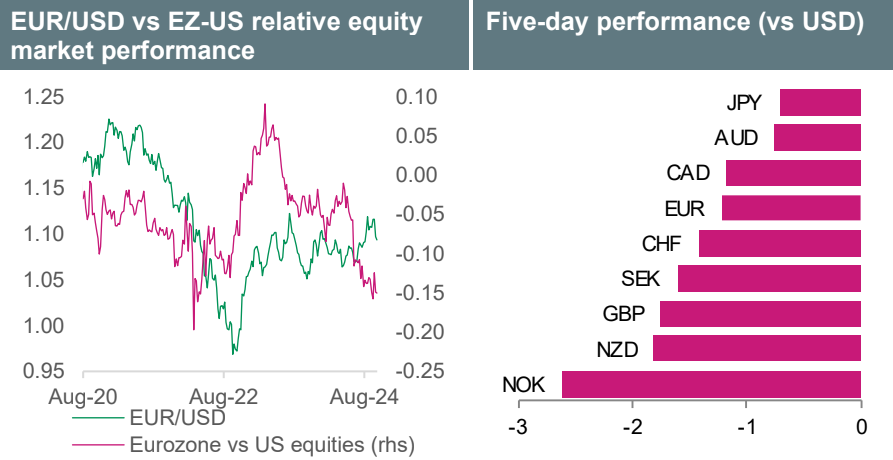

- In accounting for the US-lran deal, we have revised higher our EUR/USD forecast for Q3 from 1.12 to 1.14. The rest of our forecast profile remains unchanged, however, and we still expect the exchange rate to head lower from current levels. The USD continues to have appealing factors outside of being a safe-haven and the US being an energy exporter. The hawkish debut by new FOMC Chair Kevin Warsh has re-ignited the USD's yield appeal. We also note that the damage already wreaked by the closure of the Strait of Hormuz will hurt the Eurozone economy more than the US, and as demonstrated by the successful SpaceX IPO, investors still crave US technology stocks. Since 2020, the Eurozone vs US relative equity market performance has tended to lead EUR/USD.

- The USD's enduring appeal on growth and yield grounds will be tested in the coming week with the release of Eurozone, UK, US and Japan PMI as well as German IFO data for June. US core PCE inflation data for May as well as Tokyo CPI data for June will help determine if USD/JPY can continue challenging 2Y highs threatening further FX intervention. There will also be several ECB and Fed speakers in the coming week.

- After his victory at the Makerfield by-election, Labour Party’s Andrew Burnham is expected to soon launch his bid to oust PM Keir Starmer, and this could add to the headwinds for beleaguered GBP in the near term. Following a modestly dovish hold by the RBA, Australian CPI and labour market data will determine if markets can continue pricing out further rate hikes. Hawkish RBA Deputy Governor Andrew Hauser will speak between these two releases.