- The MPC voted 7-2 to hold Bank Rate at today’s meeting and left its guidance unchanged, reiterating that the Committee “stands ready to act as necessary” to keep inflation on track to meet the target. Bailey indicated that he is “content at the present time with holding” while acknowledging upside risks to interest rates. He framed this as consistent with a market curve that has an upward slope "accounted for more by risk premia than expected rates".

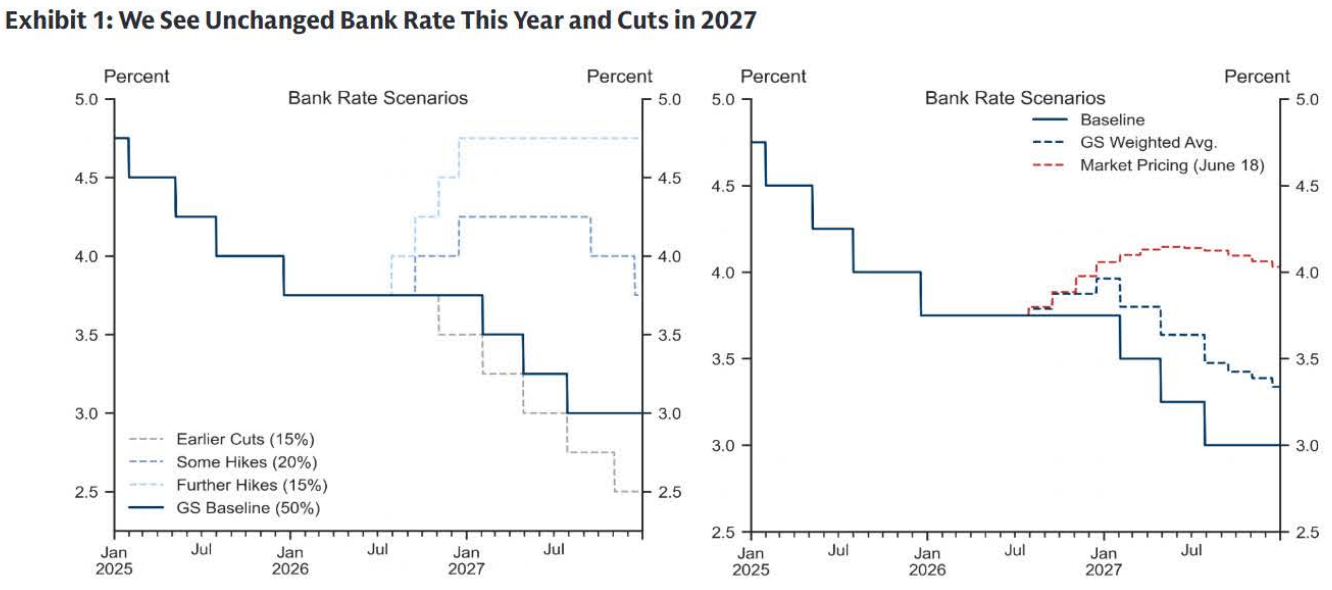

- We think that today’s communications suggest that the Committee is comfortable maintaining Bank Rate at 3.75% as things stand, while wanting to retain optionality to tighten policy if the energy shock re-escalates or if there are signs of stronger second-round effects. As such, we continue to expect the MPC to remain on hold this year if energy prices and inflation evolve in line with our forecasts. We then expect the Committee to lower Bank Rate in 2027 as labour market slack dampens the second-round effects of the shock and inflationary pressures ease.

The MPC voted 7-2 to hold Bank Rate at 3.75% at today's meeting, with Pill and Greene dissenting in favour of a 25bp hike. The vote split was in line with consensus, although we had expected that Greene would vote with the majority given recent declines in energy prices and lower inflation.

The guidance was unchanged - consistent with our expectations - with the Monetary Policy Summary indicating that the Committee will "continue to monitor closely the situation in the Middle East” and “stands ready to act as necessary" to keep inflation on track to meet the target.

Bailey in his individual paragraph noted the recent decline in energy prices - while acknowledging continued uncertainty around the situation in the Middle East - and argued that the latest data point to gradual underlying disinflation. He indicated that he is “content at the present time with holding” while acknowledging upside risks to interest rates. He framed this as consistent with a market curve that has an upward slope “accounted for more by risk premia than expected rates”.

The minutes noted that most of the other Committee members who supported a hold (Breeden, Dhingra, Lombardelli, Ramsden, and Taylor) also felt that the recent data were consistent with underlying disinflation having been “on track” before the conflict. These members also believed that upside risks to energy prices had diminished - although several emphasised ongoing uncertainty in their individual paragraphs - and noted that tighter financial conditions were “already acting to reduce inflation over time”.

One exception was Mann, who suggested that upside risks to inflation "were more prominent" but argued that there was still time to assess before raising Bank Rate given that tighter policy would have a “quick effect" on inflation. On the other side of the debate, Taylor argued that “lower rates could be preferred” if the conflict resolution holds.

The dissenters framed their votes as "part of a risk management strategy". Greene emphasised that there is “significant uncertainty" about the magnitude of second-round effects and suggested that the MPC should “insure against the possibility" that these effects turn out to be larger than expected. Pill argued that a "prompt but modest" increase in Bank Rate would leave the MPC "well-placed to address the significant uncertainties" that it faces, and so was the “most robust” policy response.

The Path Ahead

We think that today’s communications suggest that the Committee is comfortable maintaining Bank Rate at 3.75% as things stand, while wanting to retain optionality to tighten policy if the energy shock re-escalates or if there are signs of stronger second-round effects.

Our commodity strategists have recently lowered their oil price forecast and now see Brent crude at $80 per barrel at the end of the year. Given lower energy prices and downside surprises in the recent data, we have reduced our 2026Q4 headline inflation forecast to 3.3%, close to the updated BoE estimate of “a little over 314%” mentioned in the minutes. We continue to think that labour market slack will probably dampen second-round effects into pay growth, although it will take some time for the Committee to have clarity on the likely path for wages next year.

As such, we continue to think that the MPC is likely to remain on hold this year. We then expect the Committee to lower Bank Rate to 3% next year - in line with our estimate of the neutral rate - provided that incoming data including pay settlements surveys confirm our more benign view on second-round effects. Risks to our forecast remain tilted in a hawkish direction, but our confidence in our baseline has increased following the recent declines in energy prices, weaker inflation data, and the latest communications.