Deutsche Bank: The JPY - FJElite

This week has seen big cross-currents for yen. A 10% drop In oil prices, the BoJ hiking to a 31-year high but with a dovish hue, and a hawkish Fed. The upshot is that yen has weakened, taking USD/JPY exceptionally close to a four-decade high. Yen is actually the 3,d-best performer in G10 this week, so the risk of intervention may have prevented a larger fall. That seems reasonable - we see a good chance of intervention that helps yen a little in the near-term.

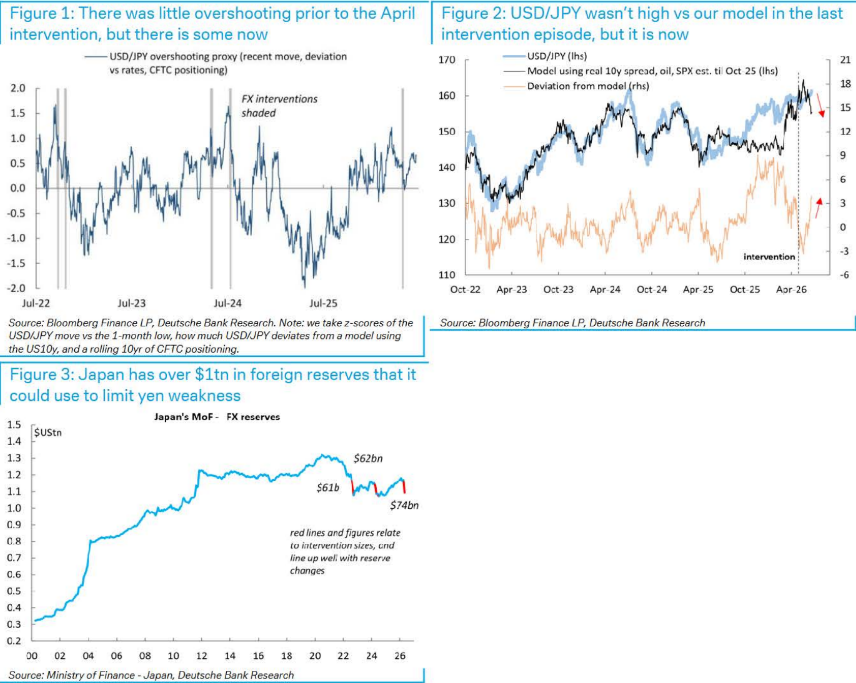

Japan was willing to intervene and spend $74bn six weeks ago when USD/JPY rose above 160. And that was despite yen weakness not looking particularly unusual. There'd been little of the 'fast move/overshoot vs fundamentals/large shorts' criteria Japan had long cited - our overshooting proxy based on these factors wasn't that high in late April (Figure 1). And a model using rates, oil and equities didn’t suggest anything particularly unusual at the time either - in fact USD/JPY was precisely in-line with fair value the day before intervention (Figure

2) . That left us to conclude that policymakers found 160+ unpalatable.

As a result a return to those levels makes us think intervention could soon come. Perhaps policymakers wanted to get past the Fed and BoJ meetings first. The firepower is certainly there - the MoF has over USSltn in foreign reserves (Figure

3) . Plus our overshooting proxy has picked up recently, and USD/JPY is getting more expensive vs our model (refer to Figure 2 and Figure 3). Of course, intervention has proven not to be a durable driver of yen strength. That would require a more hawkish BoJ and/or some action on the flows front. There's zero of the latter, and not a lot of the former either. As a result we struggle to see USD/JPY downside beyond what intervention might deliver. But we do like short EUR/JPY (which has been flat in the past month) as a trade, given the growth pulse (partly due to AI) and scope for rates repricing favors Japan.