Credit Ágricole: FX Risk Index - FJElite

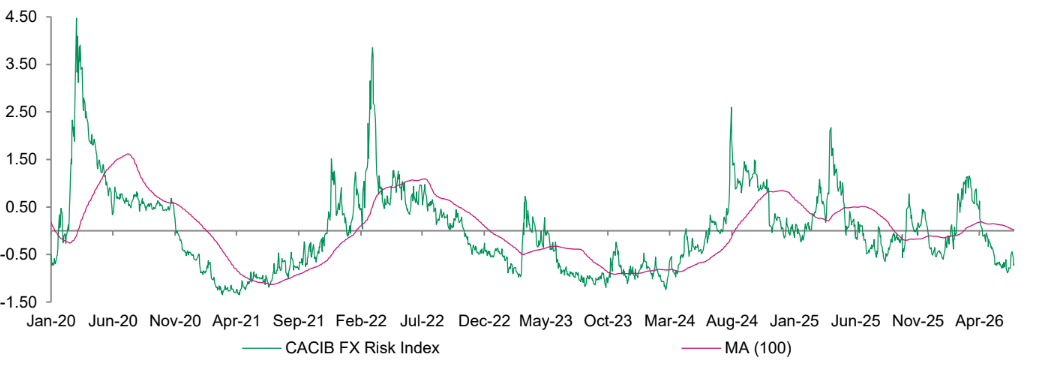

- At -0.7007 (vs -0.4940 last week) our Risk Index has dipped back towards two-year lows and the trend in the Index is nearly back in risk-seeking territory for the first time since the US-lran war started.

- Initial hiccups to the US-lran ceasefire have dissipated as both sides have agreed to stop exchanging tit-for-tat attacks and to get to the hard work of talking. Investors are looking at the flow of traffic through the Strait of Hormuz and feeling better about taking on risk.

- US cyclical data also continues to roll out on the firm side reassuring investors that the economy has not been knocked off course by higher fuel prices. The flip side to this firm growth, however, is the risk of higher US rates. Investors still feel unperturbed by rising UST yields for now.

- Risk sentiment in the coming week will be affected by new FOMC Chair Kevin Warsh’s rhetoric at the ECB Central Bank forum in Sintra. Any backing away from his recent hawkish debut would reassure risk. US ISM and non-farm payrolls data will also be watched to confirm current market assessments of the US economy and its outperformance. Events in the Middle East as well as the traffic flow through the Strait of Hormuz will also continue to receive investors' attention.

- Falling equity and FX market volatility as well as the outperformance of defensive stocks by cyclical stocks dragged our Risk Index lower over the past week. Only widening EM-Sovereign bond spreads were supporting the Index.

- Among G10 currencies, only the CHF and CAD have significant positive correlations with our Risk Index, while the GBP has a significant negative correlation with the Index. The USD’s negative correlation with the Risk Index is on the rise.