MUFG: The EUR - FJElite

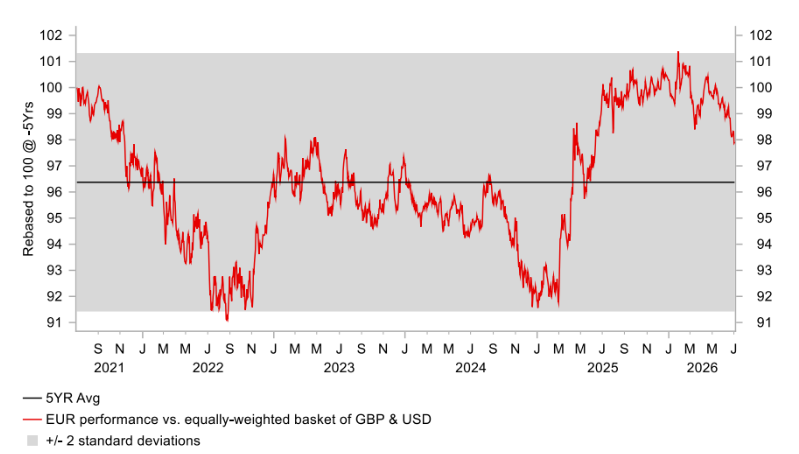

The euro has continued to trade at weaker levels overnight after the release of much softer euro-zone inflation data reinforced downward momentum. It has resulted in EUR/USD and EUR/GBP breaking below support from the bottom of their recent trading ranges at 1.1400 and 0.8600 respectively. The latest euro-zone CPI report for June revealed that headline and core slowed more than expected to 2.8% and 2.4%. When taken together with lower energy prices as well, the euro-zone economy appears to be more closely aligned with the ECB's “milder” scenario. The ECB staff projections from June revealed that headline inflation was expected to be at 3.2% in Q2 in both the baseline and mild scenarios, and core inflation at 2.4%. The latest favourable developments will dampen pressure on the ECB to tighten monetary policy further. The euro-zone rate market has become less confident that the ECB will deliver one final rate hike later this year.

ECB President Lagarde acknowledged in a panel discussion yesterday at the ECB's annual forum in Sintra that "I think the risks by the way that we have to the upside and to the downside of growth are probably more broadly balanced than they were a few weeks ago”. A downward revision to the ECB staffs inflation to the downside of growth are probably more broadly balanced than they were a few weeks ago". A downward revision to the ECB staffs inflation forecasts at the September policy meeting would be make it more difficult to communicate hiking rates further, but we still believe that one final hike remains a possibility. ECB Chief Economist Philip Lane has recently cited concerns over second round inflation effects and indicated that their estimate of the top of the range of their neutral policy rate has been raised by 25bps to 2.50%. As a result, we believe it is too soon to drop our call for a September hike although acknowledge that there is higher risk now that rates will be left on hold through the rest of this year. The recent drop in euro-zone yields and softer cyclical growth momentum in the euro-zone are contributing to a weaker euro in the near-term. After hitting a peak at 2.83% on 18th June, the euro-zone 2-year government bond yield has fallen by around by just over 30bps. A much bigger drop in yields than in the UK and Us rate markets over the same period.

Nevertheless, the less hawkish tone of President Lagarde was also evident among other panel discussion participants including BoE Governor Bailey and new Fed Chair Kevin Warsh. BoE Governor Bailey stated that “we're seeing a softening labour market. We’re seeing some softening of activity. We think we’ve got a bit of an output gap opening up”. He acknowledged as well that energy prices have 'come down quite substantially” but believes that the BoE has to be careful given the Uk has delayed reaction mechanism to energy prices so that inflation risks have not yet passed. As result, he believes interest rate cuts are still ‘off the table“. His comments are consistent with our view that the BoE are likely to leave rates on hold through the rest of this year leaving room for UK rates to continue adjusting lower.