Last week, Apple raised prices across key hardware categories, including Macs and iPads, citing higher memory and storage costs, while leaving iPhone pricing unchanged. Such adjustments are not unusual. Apple, in particular, has historically managed input cost pressures through pricing, product mix and configuration upgrades. From that perspective, the move can be read as a standard margin management decision rather than a shift in underlying demand or pricing power. The more relevant question is whether the underlying cost pressures are cyclical or structural.

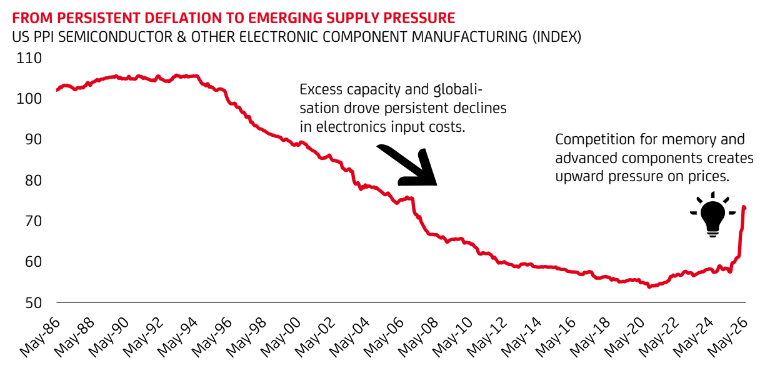

The AI capital spending cycle suggests that the transition may prove more inflationary than commonly assumed, at least temporarily. Hyperscalers are committing unprecedented levels of capital expenditure to data centres - potentially exceeding USD 700bn this year alone - absorbing an increasing share of global supply of advanced semiconductors, high-bandwidth memory and networking equipment While supply will respond over time, near-term capacity remains constrained. This is beginning to show up in pricing dynamics. Electronic-component deflation, long a structural feature of consumer hardware, has stalled as Al-related investment accelerates. The relationship is consistent with a regime in which investment demand increasingly competes with consumer demand for finite inputs.

Kevin Warsh, the new Federal Reserve chair, has argued that AI is likely to prove structurally disinflationary, drawing explicit parallels to the late-1990s productivity boom. He has described AI as a “significant disinflationary force" that should lift productivity, lower costs and increase real incomes over time. That remains a plausible end-state. Al-driven productivity gains should, over time, expand supply, reduce marginal costs and exert downward pressure on inflation.

However, the path to that outcome may be less benign. The infrastructure required to support AI at scale is highly capital-intensive, while operating increasingly powerful models demands ever more energy and computing capacity. Together, these forces could create an inflationary impulse before the technology’s productivity benefits are fully realised. Apple’s pricing action is therefore best viewed as a marginal data point within a broader trend: cost pressures associated with the AI ecosystem are beginning to extend beyond enterprise IT supply chains.

For investors, this matters because it shapes where value is created during the transition. Companies exposed to the infrastructure underpinning AI adoption, as well as those with durable pricing power, remain well positioned as the build-out continues. Equity markets have reflected this dynamic, favouring beneficiaries of rising capital expenditure across compute, memory, networking and power infrastructure. The risk, however, is that investors are pricing Al's long-term productivity gains more confidently than the inflationary pressures that may accompany the investment cycle required to achieve them.