Goldman Sachs: The USD - FJElite

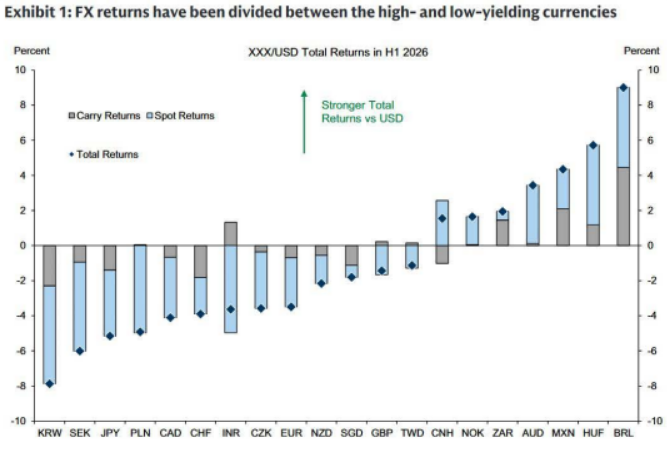

USD: Division to grow wider. The forces that have combined to strengthen the Dollar over the last few months look increasingly likely to endure. We came into 2026 projecting less-exceptional US performance, and a weaker Dollar over time. Since then, the US Dollar has benefited from twin economic shocks—an AI boom and an energy supply bust—that have combined to raise the relative profile of US assets yet again. The Al boom has raised capital expenditures and inflationary pressures at least in the short term. Most notably for FX, and as Chairman Warsh highlighted in Sintra this week, this is unique to the US among the DM economies. The realization of higher spending plans, and the ensuing Fed debate around whether to respond, has shifted rate differentials—particularly the market-implied neutral rate—in the Dollar’s favor. Taken together, these developments have quieted investor calls to diversify away from US assets, which was an amplifying force behind the Dollar’s depreciation a year ago. It follows that Dollar performance this year has been divided along these lines—rising against low-yielders and falling against currencies offering higher carry (Exhibit 1). There are clear risks that could threaten this trend in both directions in the months ahead. As we discussed last week, we see downside risks stemming from more balanced activity and policy prospects or a re-emergence of the credibility concerns that undermined the Dollar’s high valuation last year. On the other hand, confirmation that more restrictive policy is required could lead to outsized FX moves if policy diverges even more than currently discounted by markets. Our baseline is instead that US performance should be sufficiently solid for the rate differential to narrow only slightly, despite our more dovish Fed call, and investor demand for US assets to be stronger than last year. And we think CNH, which was the notable exception to the high vs. low yielder trend in H1, should continue to benefit from firm policy support, which limits the scope for broad Dollar appreciation. For much of the past few months, we have said that economic trends should support the Dollar against low yielders on a tactical horizon, and revised our forecasts in that direction in mid-March. We increasingly think these forces look likely to linger for longer, and we are unlikely to return to broad-based, sustained Dollar depreciation for some time. To reflect an ongoing divided Dollar environment, we are revising our forecasts for EUR/USD to 1.14, 1.12 and 1.12 in 3,6 and 12 months (from 1.14,1.18 and 1.20 previously). We have also revised our forecast path for USD/JPY to 162,163 and 165 (from 160,