Goldman Sachs: The JPY - FJElite

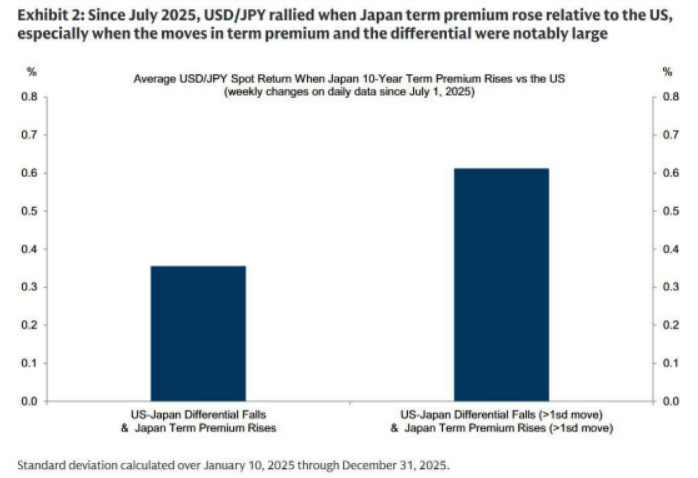

JPY: Revising up our USD/JPY forecasts. The Japanese Yen recently traded to its weakest level versus the US Dollar in 40 years, keeping the MoF focused on the exchange rate and seemingly ready to conduct JPY-buying operations again. In fact, the latest reports suggest that the MoF may end the final warnings ahead of official operations to further discourage short positioning. But the broader macro backdrop of higher-for-longer US yields, low recession risk, lingering fiscal concerns, and only gradual BoJ hikes strongly argues for continued depreciation pressure on the currency. That explains the relatively quick return to an upward trend in USD/JPY within weeks of the last operations—echoing the aftermath of the April 2024 intervention and implying a similar outcome if additional operations occur soon. In fact, we see no reason for the upward trend in USD/JPY to stop without an unexpected negative US growth shock or a BoJ pivot towards more aggressive policy tightening. Otherwise, growing market concern about inflationary / fiscal pressure in Japan on the back of the government’s stimulus plans should continue to push up term premium in JGB yields relative to US Treasury yields. Over the past year, in weeks when Japan term premium increased versus the US, USD/JPY rose by roughly 0.35% on average—and closer to 0.60% on average when the move was greater than 1 standard deviation in both Japan term premium and the differential (Exhibit 2). We expect that dynamic to continue. Intervention can slow the move and buy time for a potential shift in the macro that then leads to sustained Yen appreciation. But without that, the impact ultimately proves short-lived with diminishing effect, and we think that either a recession or more rapid BoJ hikes look unlikely over the coming year. That implies that the trend higher in USD/JPY should extend, even if there are additional rounds of intervention that successfully reset the exchange rate to lower levels and suppress vol for some time. Therefore, we have revised up our forecasts to 162,163,165 in 3,6,12 months (vs. 160,158,155 previously). We also continue to favor using JPY as a funder for high-carry EM expressions, alongside other low-yielding G10 currencies.