Credit Ágricole: FX Weekly - FJElite

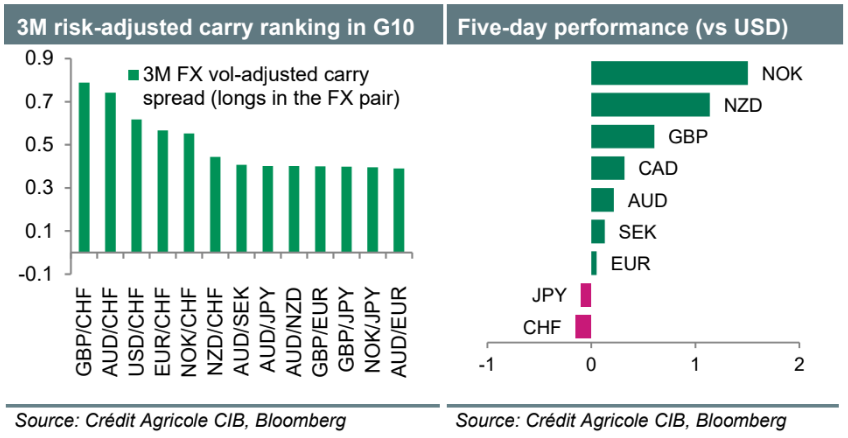

- The latest escalation of geopolitical risks in the Middle East has had little impact on G10 FX vols and left them stuck at six-year lows. FX investors seem to expect another Trump Always Chickens Out or TACO trade that could see the US-lran tensions subside soon. Our seasonality analysis further suggests that the summer lull could keep FX vols low in July. Low vols, in turn, support FX carry trades and have pushed our in-house FX carry performance indices to record highs recently. Our ranking of FX vol-adjusted carry spreads signals at present that longs in GBP, AUD and USD funded in CHF are among the most attractive FX carry trades.

- The USD remains the high-yielding, safe-haven King of G10 FX. Its rate appeal should keep it supported vs funding currencies like the JPY, CHF and EUR. It would take higher FX vols, however, to prop up the USD vs other high yielders. With FX carry trades still dominant, the near-term G10 FX market outlook would depend on the level of FX vols and the evolution of the central bank policy outlooks. The return of US-lran tensions is worrisome, but it is unclear whether it could trigger a fullblown risk aversion and FX vol spike. Japanese officials have recently called on the GPIF to invest more locally. The latter would have to perform an interim review, leaving FX investors on high alert for any announcement that may darken the outlook for JPY-funded carry trades.

- Focus next week will also be on the testimony of Fed Chair Kevin Warsh before US Congress as well as the US CPI and retail sales data for June. Warsh’s views on the economy and whether the Fed should look through the Al-investment-led inflation spike could attract a lot of attention. The inflation data could show signs of abatement too and ease the pressure on the Fed to hike rates. Provided that Fedspeak and US data offset the impact of geopolitical risks and help ease financial conditions, FX carry trades could remain in demand and FX vols could stay close to the lows.

- Domestic politics have become a key market driver in Europe once again after a court ruling allowed National Rally’s Marine Le Pen to run in the 2027 French presidential elections. Focus will also be on the transfer of power from outgoing UK PM Keir Starmer to his successor Andy Burnham. Elsewhere, the May UK GDP data could highlight that the economy remains feeble, in a blow to the high-yielding GBP. The BoC is set to keep its policy rate unchanged at 2.25% and to stick to its flexible two-way stance. That said, we do not concur with North American money markets pricing in an increasing BoC policy lag relative to the Fed.