Credit Ágricole: FX Weekly - FJElite

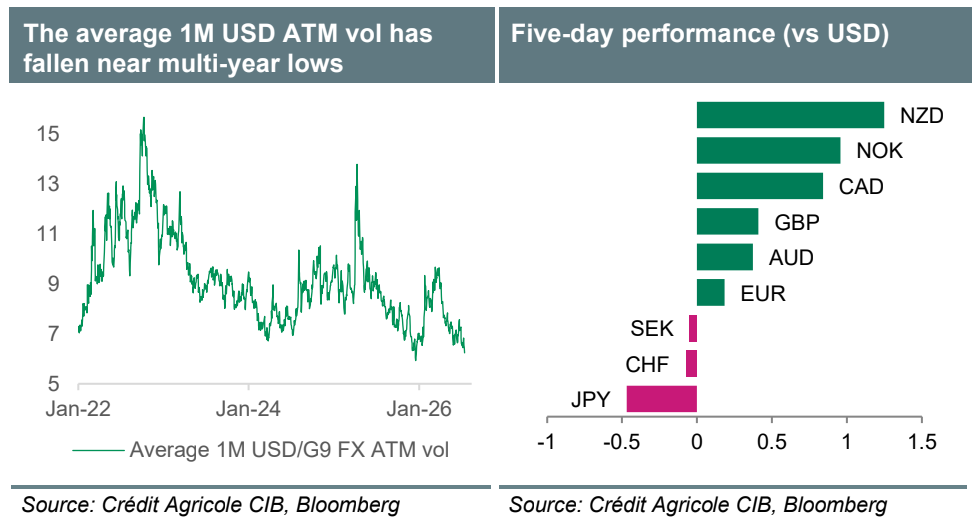

Military clashes have resumed between the US and Iran over the past week, sending oil prices higher and subsequently reigniting the prospects of extra monetary tightening. For the Fed, a sizeable miss in US CPI has offset that, even though Chair Kevin Warsh was quick to caution that it does not mean mission accomplished yet. The FX market reaction has so far proved fairly subdued, with FX majors still treading water this month and hardly any sign of a change in command as per the sanguine pricing of front-end FX vol.

Nevertheless, many pitfalls still loom on the immediate horizon, and therefore any unexpected setback could risk causing larger moves across G10 FX. Overall, the USD could continue to follow the price action in the US rates markets and the resilience of risk sentiment. The latter would depend on how a fragile equilibrium in the Middle East evolves. Next week’s expiry of the global 10% US tariffs could also refocus market attention onto the US trade policy. The recent announcement of 25% duties on some Brazilian imports may revive the concerns of a greater toll on global trade, while the US Treasury has on its side had to deal with deteriorated fiscal revenues due to the growing refund of the so- called reciprocal tariffs. That said, we continue to think that it would take further escalation of geopolitical and trade risks to upset the summer lull. FX carry trades could remain a dominant FX market driver and leave the USD vulnerable vs other G10 high-yielders but supported vs low- yielding G10 currencies.

The ECB should keep its rates unchanged in July but remain vigilant on the outlook for Eurozone inflation, keeping markets expecting more hikes ahead. EUR investors will also focus on the quality of the latest business confidence data. For the EUR to gain ground, its relative rate disadvantage would have to shrink further and erode its appeal as an FX carry funding currency. Elsewhere, fears over the UK fiscal outlook have eased after recent reports that Shabana Mahmood could be the new Chancellor. In the near-term, the GBP could continue to benefit from its appeal as a carry investment currency and take its cue from the path of UK rates and sovereign CDS spreads. Many positives linked to abating fiscal risks and hawkish BoE rate expectations are already in its price, however, and the GBP could struggle to extend its recent gains.