MUFG: Some Signs of Homeward Bias Already - FJElite

The yen remains close to cyclical lows and the US data yesterday (see below) along with the risk of further crude oil price rises are curtailing the appetite to sell the US dollar following the weak CPI and PPI reports. We would still argue that the lack of price action in the yen should not be viewed as the government’s push to encourage greater investment in domestic assets not being significant. We would still argue that it marks a notable turning point from the Abenomics era that encouraged investments in risker assets to boost returns - for pensions this would help restore confidence in Japan's pension system and in turn reduce cautionary savings. That would lift consumer spending and help end mild deflation.

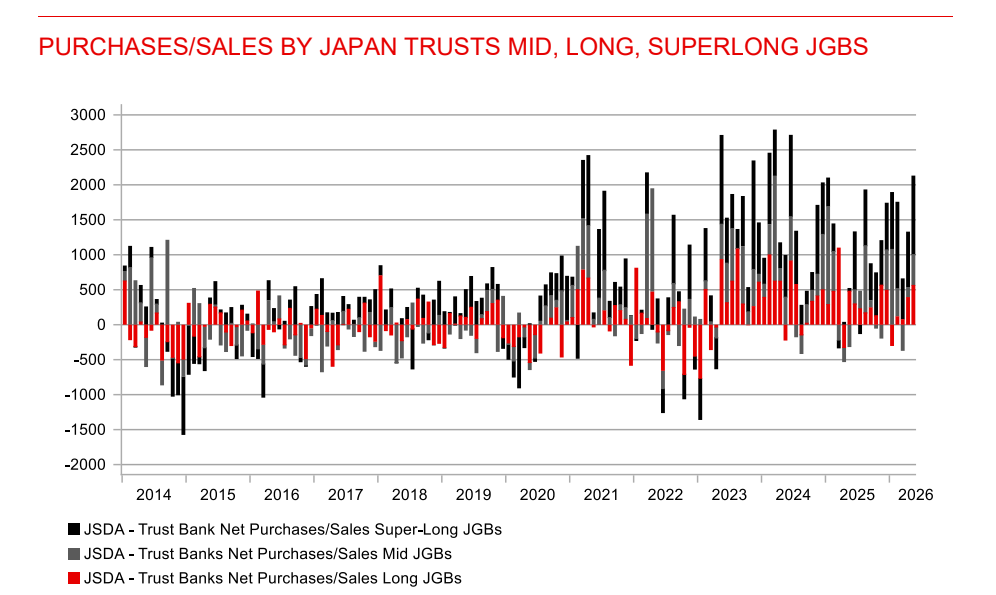

The start of formalising the end of that policy - which is happening now - is significant. It could certainly help shift the mindset on investment behaviour. There is though some evidence that flows have already started to shift. Below is the JSDA data on JGB buying by Japan Trusts (that would include GPIF). You can see a clear upturn in buying from late 2020, which continued bar a disruption in 2022 possibly reflecting greater volatility during the global inflation shock period. From the Abenomics review and announced change in 2014 (Domestic bond allocation reduced from 60% to 35%) Trust banks started selling JGBs - over the five-year period 2014-18 Trusts sold JPY 1,280bn worth of JGBs. The GPIF allocation for domestic bonds was then lowered from 35% to 25% in 2020 but the composition was already slightly below 25% (there was a +/-10% band then) and this in fact looks to have in fact marked a turning point back favouring JGBs although the notable pick-up in JGB buying was from 2021.